Why CBDCs are the “Sovereign Operating System” for Money

What are Certified Bank Deposit Coins?

If stablecoins are the “Internet Protocol” for money—privately built and open-source—then CBDCs (Central Bank Digital Currencies) are the “State Operating System.”

While the private sector was busy building the digital dollar through the GENIUS Act, the world’s central banks were quietly constructing their own version of the future. A CBDC isn’t just a digital token; it is the national currency itself, in digital form, sitting directly on a government ledger.

What is a CBDC? (The “State Money” Model)

At its simplest, a Central Bank Digital Currency (CBDC) is a digital version of a country’s national currency, issued and backed directly by the central bank.

Unlike the money in your bank account today—which is technically a “private” liability of a bank like Chase or Barclays—a CBDC is a “public” liability of the government, exactly like the physical paper cash in your wallet.

Why They Matter in 2026

We have reached the “Great Bifurcation.” The global financial map is now split between nations leaning into Private Stablecoins (the US model) and those doubling down on State-Issued CBDCs (the China and EU model).

The Death of Anonymity: CBDCs represent the final transition from “Physical Cash” (untraceable) to “Programmable Cash” (fully auditable).

The Fed’s Red Line: In a historic move this past July, the US passed the Anti-CBDC Surveillance State Act, effectively blocking the Federal Reserve from issuing a retail digital dollar. This has made the US the global champion of private digital dollars, while the rest of the world builds public digital rails.

How They Work

CBDCs are engineered for two entirely different purposes, often referred to as the “Wholesale” and “Retail” split:

1. Wholesale CBDCs (The “Back-End” Ledger)

These are designed for the “plumbing” between banks. Instead of banks taking three days to settle a trade, they use a shared central bank ledger to settle billions of dollars in milliseconds.

The Hook: It eliminates “Settlement Risk.” In 2025, projects like mBridge (connecting China, UAE, and others) proved that countries can trade directly without needing the SWIFT system or a US correspondent bank.

2. Retail CBDCs (The “Citizen” Wallet)

This is a digital version of the money in your pocket, issued directly by the central bank to you.

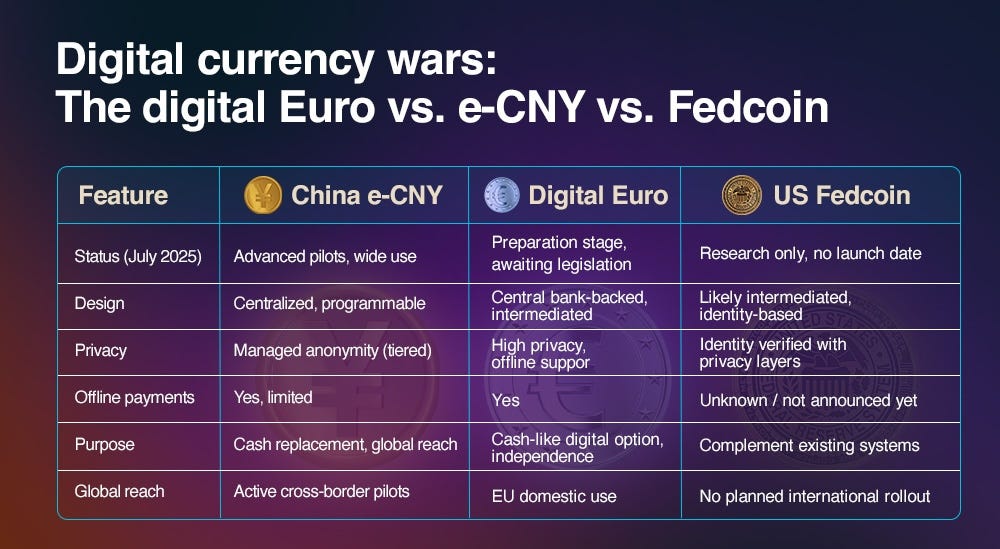

Examples: China’s e-CNY (Digital Yuan), Nigeria’s e-Naira, and the upcoming Digital Euro (slated for a 2027 pilot).

The Hook: You don’t need a bank account at a private bank like Chase or Barclays. Your “account” is with the government. It’s the ultimate “Financial Inclusion” tool—but it comes with a catch.

The Great Divide: Control vs. Freedom

The biggest story of 2026 is the philosophical war between the Digital Yuan and the Regulated Stablecoin.

1. China’s “First Mover” Domination

As of late 2025, China’s digital yuan (e-CNY) has processed over $2 trillion in volume. It isn’t just for buying coffee; it is being used to pay government salaries and settle international oil contracts.

The Shift: China is using its CBDC to bypass the US-led financial system entirely, creating a “Fortress RMB” that sanctions cannot easily touch.

2. The Digital Euro: Europe’s Third Way

While the US says “No” to CBDCs and China says “Yes,” Europe is trying to find a middle ground. The European Central Bank (ECB) is finalizing the Digital Euro framework for 2026.

The Goal: To give European citizens a public digital payment option so they aren’t 100% dependent on American tech giants like Visa, Mastercard, or PayPal.

3. The US “Private” Counter-Attack

By banning a federal CBDC and passing the GENIUS Act, the US has essentially “outsourced” its digital currency to companies like Circle and Paxos. The US bet is simple: The private sector will innovate faster than a government bureaucracy ever could.

Real-World Applications (and Implications)

Direct Stimulus: During the next economic cooling, a government with a CBDC won’t mail checks. They will “airdrop” digital cash directly into your government wallet.

Programmable Spending: A CBDC can have an “expiration date.” To stimulate the economy, the government could issue $500 that must be spent within 30 days, or it disappears.

Instant Taxation: Imagine a world where sales tax is deducted from a merchant’s wallet the exact second a transaction happens. No more filing; the state just takes its cut in real-time.

Sanction Proofing: Countries can trade “Peer-to-Peer” at a state level, making the traditional “weaponization of finance” through bank freezes much harder to enforce.

The Risks

The convenience of a CBDC comes with the ultimate price: The end of financial privacy.

The Panopticon: Every transaction you make is visible to the central bank. There is no “off-ledger” digital cash in a CBDC world.

Social Credit Linkage: In a retail CBDC system, your ability to spend money could theoretically be linked to your behavior. (e.g., “You haven’t paid your parking tickets, so your digital wallet is restricted from buying plane tickets.”)

Disintermediation: If everyone moves their money from a “risky” private bank to a “safe” central bank wallet, private banks could collapse, ending the traditional lending system as we know it.

Key Takeaways

CBDCs = Sovereignty + Control. They are the government’s answer to the “threat” of crypto and stablecoins.

The World is Splitting. The West is moving toward Private/Regulated digital money (Stablecoins), while the East is moving toward Public/State digital money (CBDCs).

Programmability is the Future. Whether it’s a stablecoin or a CBDC, the days of “dumb money” are over. Money is now code.