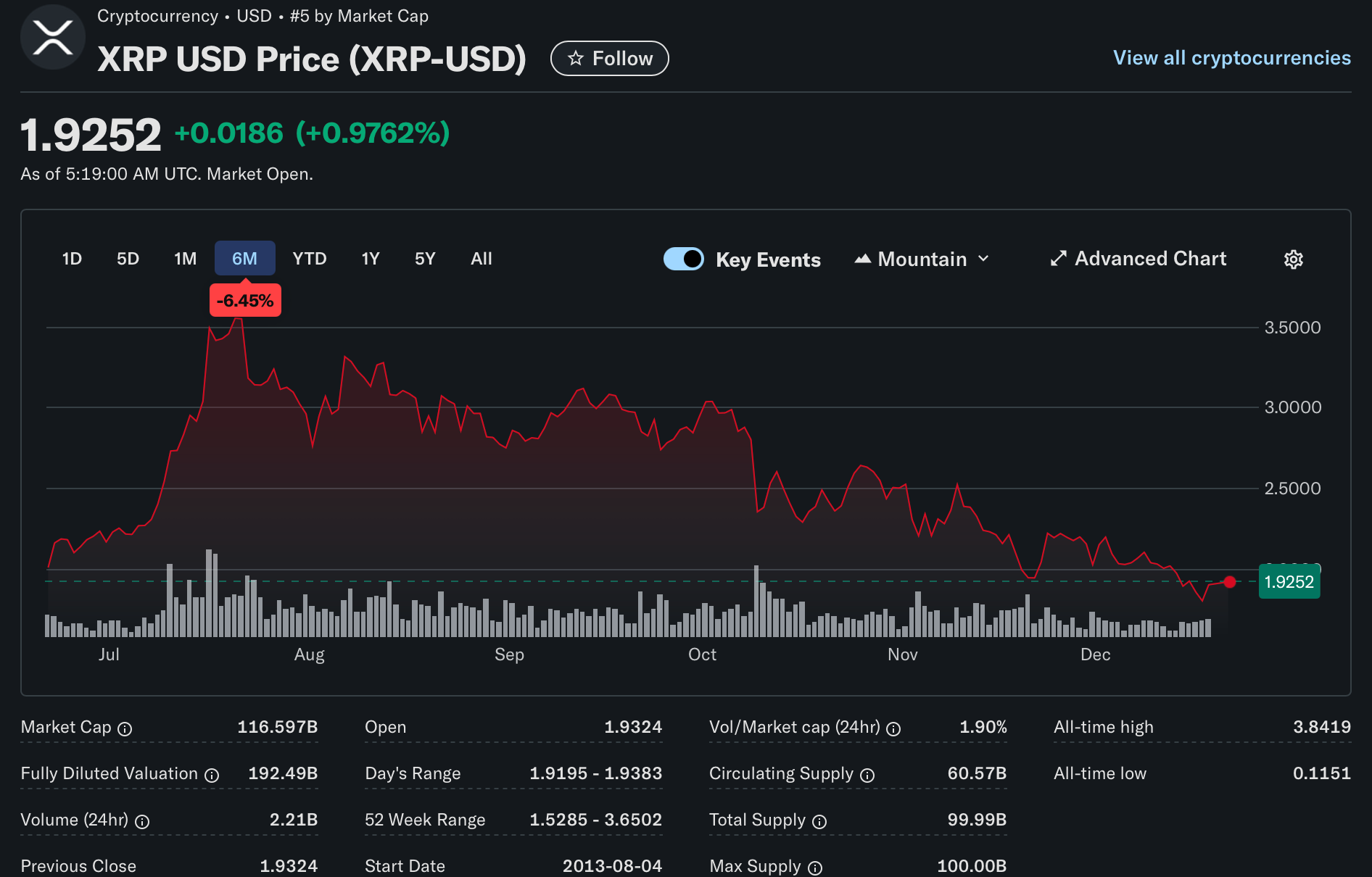

In the world of blockchain, few assets are as polarizing as XRP. While its proponents view it as the “Godzilla of Finance” destined to replace the aging SWIFT system, critics argue it is a solution in search of a problem. To understand this debate, one must distinguish between the technology (RippleNet) and the asset (XRP).

What XRP Aims to Offer: The “Bridge” to Instant Liquidity

XRP was designed with a singular, industrial-grade purpose: to act as a bridge currency for international payments.

Currently, the global financial system relies on a “nostro/vostro” model. For a bank in the U.S. to send money to a bank in Mexico, they must keep pre-funded accounts in Mexican Pesos (MXN) to ensure liquidity. This traps trillions of dollars in idle capital globally. XRP aims to solve this through On-Demand Liquidity (ODL):

Speed: While traditional SWIFT transfers can take 3–5 days to settle, XRP transactions settle in roughly 3–5 seconds.

Cost: By using XRP as a bridge, banks can avoid the high fees of intermediary correspondent banks. XRP transaction fees are typically less than a fraction of a cent.

Capital Efficiency: Banks would no longer need to “pre-fund” foreign accounts. They can hold their local currency, buy XRP, send it, and have it converted to the destination currency instantly.

The Counter-Argument: Why “No One Needs It”

The argument that XRP is unnecessary is not an attack on Ripple’s technology, but rather a critique of the token’s role within that technology. Here is the factual basis for why the finance industry might bypass the token:

1. The Technology Doesn’t Require the Token

Ripple’s primary software, RippleNet, allows banks to send messages and settle payments faster and more transparently than SWIFT. Crucially, banks can use RippleNet without ever touching XRP. They can use the protocol to settle in traditional fiat (USD, EUR) or even private stablecoins. In fact, the vast majority of Ripple’s early institutional partners used the “xCurrent” product, which does not require the XRP token.

2. The Rise of Stablecoins and CBDCs

XRP’s “bridge” utility is being squeezed by more stable alternatives.

Stablecoins: Regulated assets like USDC offer the same 24/7 settlement benefits of blockchain without the price volatility of XRP.

CBDCs: Central banks are developing their own Central Bank Digital Currencies. If the Federal Reserve and the European Central Bank create digital versions of the Dollar and Euro that can talk to each other directly, the need for a third-party “bridge” like XRP effectively vanishes.

3. Volatility Is a Barrier to Entry

For a bank to use XRP for a $100 million transfer, it must navigate the asset’s volatility. If the price of XRP drops 2% during the few seconds it takes to “bridge” the transaction, the bank loses a massive amount of money. While Ripple offers tools to mitigate this, most conservative financial institutions find it simpler to move “digital dollars” rather than a speculative cryptocurrency.

4. The Concentration of Supply

A significant portion of the total XRP supply is still held in escrow by Ripple Labs. Critics argue this creates a “centralization” risk that traditional finance (TradFi) is uncomfortable with. If a single private company can influence the market by releasing or withholding billions of tokens, it lacks the neutral, decentralized appeal of an asset like Bitcoin or the legal backing of a government-issued currency.

The survival of XRP depends on whether Ripple can prove that ODL (using the token) is significantly cheaper than using stablecoins or CBDCs. As of 2025, the industry is leaning toward stable, regulated assets over volatile bridge tokens.