The economic strategy now unfolding in the U.S. may look bold and unprecedented, but it’s actually a continuation of an old pattern. From Truman to Nixon to today, every administration facing overwhelming national debt has reached for the same core playbook:

manage debt through controlled debasement

stimulate nominal growth

preserve public confidence while quietly eroding the real burden of what’s owed.

The Modern Revival of an Old Strategy

Trump’s policies—tariffs, reshoring, energy expansion, and investment incentives are framed as nationalist and pro-growth, but their underlying mechanics echo the postwar approach of Truman and Eisenhower:

Keep real interest rates negative to make debt cheaper over time.

Drive nominal GDP growth through industrial policy and tariffs.

Tolerate moderate inflation to quietly dilute liabilities.

Maintain confidence in the currency and the system that supports it.

The difference is that Truman hid this policy behind postwar recovery. Trump presents it as patriotic reindustrialization—a fiscal necessity turned into political theater.

Historical Parallels

Truman & Eisenhower (1940s–1950s)

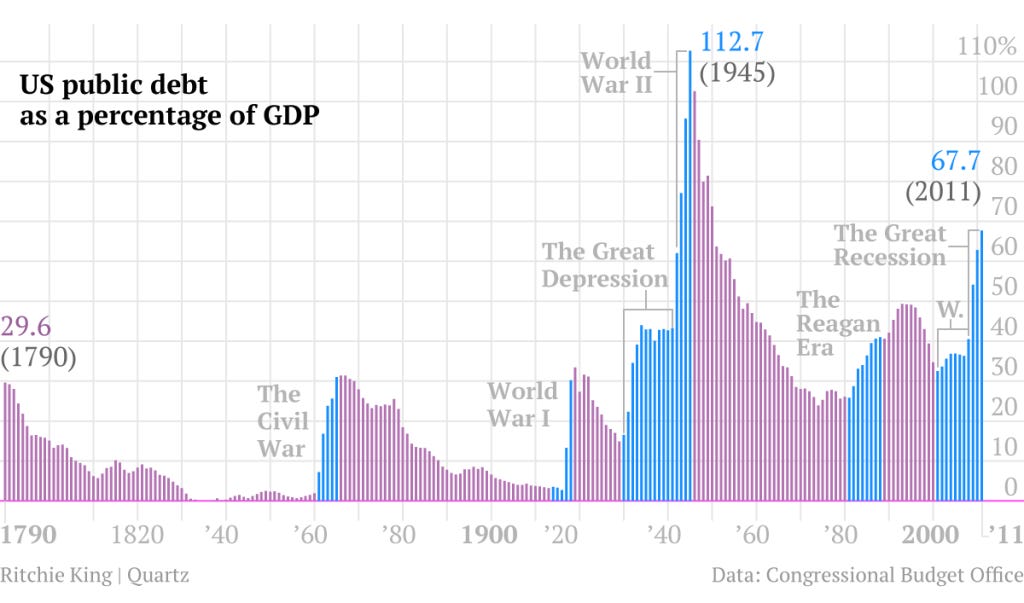

U.S. debt soared from 40% of GDP (1941) to ~120% (1945) due to WWII spending.

Truman’s 4-part solution:

Keep rates low (with Fed cooperation)

Maintain nominal GDP growth

Allow moderate inflation

Implement high top marginal tax rates (up to 91%)

The result: debt deflated in real terms, inflation eased the burden, and confidence remained high.

Nixon (1970s)

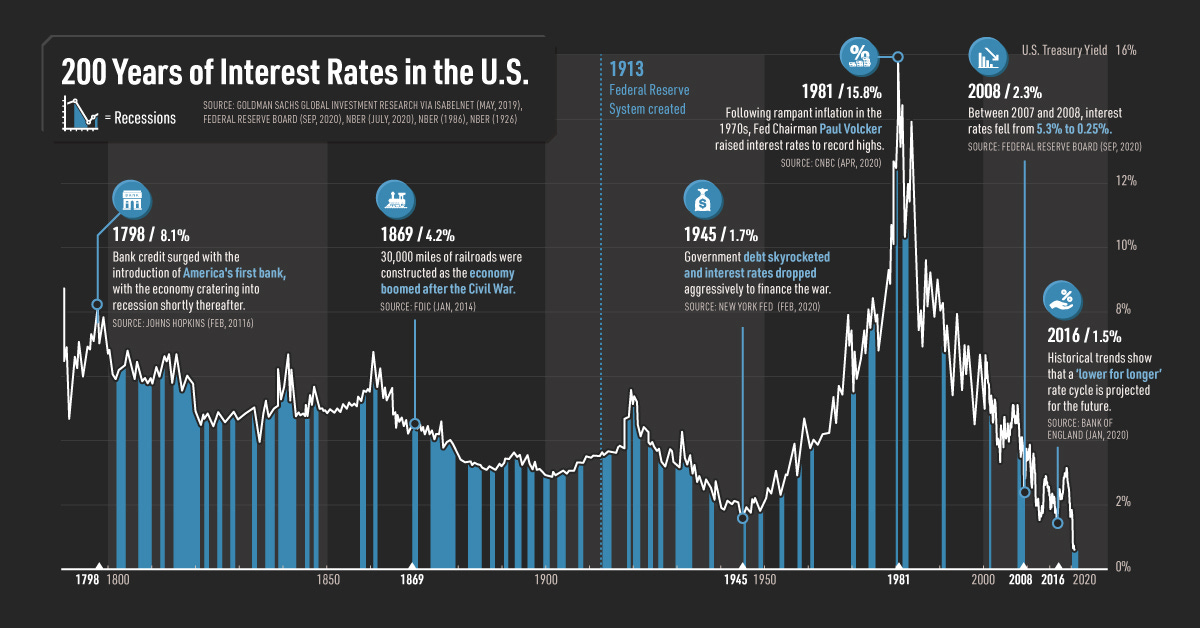

Ended the Bretton Woods system, severing the gold peg and allowing a floating dollar.

Protected U.S. reserves while gaining flexibility to manage debt through monetary policy.

The goal was unchanged: reduce debt’s real weight while maintaining economic growth.

Trump (2020s)

National debt again exceeds 120% of GDP, echoing post-WWII levels.

The same levers are being pulled:

Low rates (via political pressure on the Fed)

Tariffs and domestic investment to boost nominal growth

Tolerated inflation to erode debt value

Tax cuts to drive private investment and maintain momentum

The difference: there is no gold peg to defend. The dollar’s credibility itself is the peg.

The Big Picture Pattern

Across eight decades, the U.S. debt-management strategy has repeated in nearly identical form:

Run up debt (war or stimulus spending).

Keep rates low (then via pegging; now through policy pressure).

Stimulate demand (then pent-up postwar; now through fiscal incentives).

Let inflation run (to shrink the debt burden).

Drive nominal GDP growth (to improve the ratio).

Roll debt cheaply (refinance at low nominal yields).

Normalize later (tighten policy once the optics improve).

The outcome is always the same: real wealth shifts from savers to borrowers, and from labor to capital. The government’s balance sheet improves—not through austerity, but through dilution.

Why It Matters Now

The risk today is not gold outflows, as in Nixon’s time. It is a loss of global confidence in U.S. bonds and the dollar itself. The structure of the system depends on belief in the dollar as the safest store of value. Every round of controlled inflation tests that faith.

Understanding this playbook reframes today’s policies as part of a much longer continuum—not reckless improvisation, but a deliberate continuation of how America has always managed debt crises.

Positioning for the Cycle

In environments like this (where inflation is tolerated and real rates are suppressed) nominal returns can mislead. Asset prices rise, but the currency beneath them weakens.

Historically, the beneficiaries are clear:

Real assets (land, commodities, infrastructure)

Resilient equities with tangible productivity

Inflation-linked instruments (TIPS, hard commodities)

Those most exposed:

Bonds and cash, which lose purchasing power quietly and predictably.

How It Works in Practice

By engineering nominal growth through tariffs, infrastructure projects, and energy expansion, the government creates the appearance of prosperity while quietly transferring the debt burden to savers and wage earners.

This structure rewards:

Borrowers and asset holders (their debts shrink in real terms)

The government itself (its liabilities erode through inflation)

And punishes:

Cash holders and fixed-income investors (their purchasing power decays)

What to Expect

Over the next decade, the U.S. will likely replay a familiar cycle—nominal expansion masking real erosion. The mechanisms are subtle, but the outcomes are predictable:

Phase 1: Stimulus and Surge

Fiscal expansion, tariffs, and industrial policy drive visible growth. Markets perform well in nominal terms as liquidity expands and real rates remain negative.Phase 2: Inflation and Transfer

The debt burden lightens as inflation outpaces interest costs. Savers, bondholders, and wage earners quietly absorb the loss, while borrowers, asset owners, and the government benefit from the dilution.Phase 3: Normalization and Tightening

Once the debt-to-GDP ratio appears contained, policymakers will shift toward tightening—talking up “fiscal discipline” to restore confidence. Nominal yields may rise modestly, but not enough to reverse the real erosion already done.

Throughout this process, Treasury yields will stay artificially low, foreign holders will continue diversifying into hard assets, and domestic investors will seek refuge in real assets, productive equities, and commodities.

The surface narrative will be one of prosperity and recovery. But in real terms, it will represent a quiet revaluation of money itself—a slow exchange of purchasing power for stability.

The Takeaway

What appears as a resurgence of American industry is, beneath the surface, a managed reset of the dollar’s real value. Every prior debt cycle has relied on the same silent trade: exchange purchasing power for political and economic continuity.

This time, the process is transparent. Inflation is tolerated, growth is manufactured through policy, and confidence is sustained by narrative rather than backing. The dollar is no longer pegged to gold or productivity—it is pegged to belief.

For investors and policymakers alike, the lesson is the same: nominal gains mean little when the denominator is dissolving. Real wealth in this era belongs to those who anchor themselves to scarcity—land, commodities, productive assets, and the capacity to generate value independent of fiat strength.

The Great Debasement is not a future event; it is the system functioning exactly as designed. The challenge now is not to predict collapse, but to recognize the quiet arithmetic of preservation playing out in real time.