The Bubble Question Is the Wrong Question

Why rotating to “safety” may be a bigger bet than staying invested

Lately, more investors have been asking some version of the same thing:

Is this a bubble?

The question usually arrives with a reference point — sometimes explicitly to Michael Burry, sometimes just implicitly to past manias. Tech concentration. Passive flows. AI multiples. Government debt. Take your pick.

The framing is familiar. It suggests a familiar outcome: excess, collapse, reset.

But this moment does not behave like prior bubbles. And treating it as one may be more misleading than helpful.

What Is a Bubble?

Before asking whether we are in one, it helps to be precise about what a bubble actually is.

A financial bubble is not simply “high prices” or “widespread optimism.” Those conditions exist in many healthy markets.

A bubble has a more specific structure. At minimum, it involves:

A discrete object of speculation

A sector, asset class, or theme that can be clearly isolated.Prices detached from plausible cash flows

Valuations rely on narrative acceleration rather than realizable economics.Marginal buyers driven by expectation, not utility

Purchases are made primarily because prices are rising.A funding or belief shock that removes the marginal buyer

Liquidity dries up, sentiment shifts, or capital costs rise.A repricing that corrects the excess without breaking the system

Losses are concentrated. The broader framework survives.

Crucially:

Bubbles burst, but systems remain intact.

That distinction matters.

Bubbles Are About Mispricing. This Is About Belief

Classic bubbles share a familiar profile:

identifiable excess

speculative leverage

a narrative untethered from cash flow

a discrete object that can reprice downward

Think dot-com stocks, housing tranches, SPACs, meme equities.

This cycle feels different because what people are reacting to is not one asset, but the entire framework in which assets are priced.

Today’s discomfort is less about “stocks are expensive” and more about a quieter question:

Do we still believe the system will behave the way it always has?

That question is ideological, not analytical.

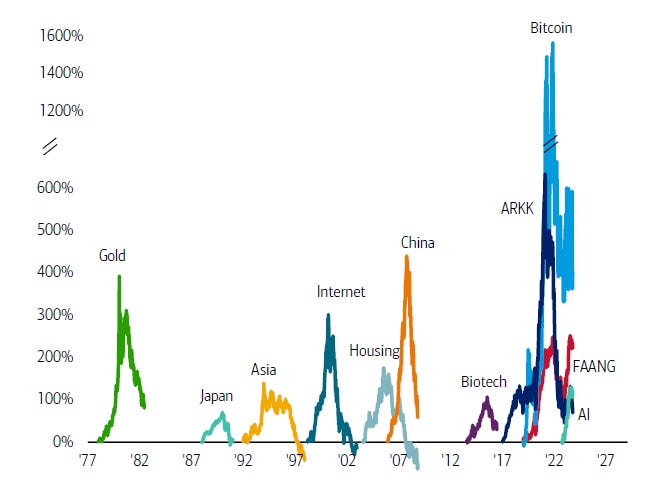

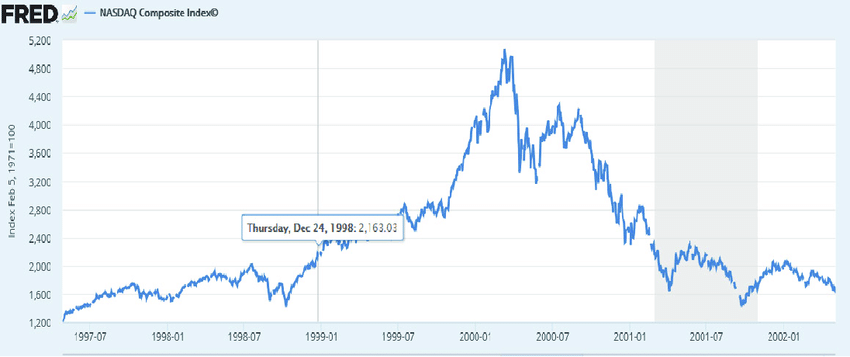

The Dot-Com Bubble as a Reference Case

The late-1990s dot-com era fits the classical definition of a financial bubble and is often used as the default comparison.

Key features included:

speculation concentrated in a narrow slice of equities (internet and tech)

valuations untethered from near-term cash flows

capital allocated based on narrative (users, eyeballs, total addressable markets)

marginal buyers driven by momentum, not utility

When belief broke, prices corrected sharply. The NASDAQ Composite peaked in 2000 and fell nearly 80% over the following two years.

Crucially, the damage was contained:

the internet survived

the financial system remained intact

capital rotated rather than disappeared

investors could exit the excess without rejecting the broader framework

That containment is what made dot-com a bubble — and why it remains a useful, but limited, comparison.

The Implicit Bet Everyone Is Already Making

Whether investors admit it or not, the modern market rests on a bundle of assumptions:

liquidity will be provided when needed

deficits can expand without immediate consequence

passive flows will continue to dominate price discovery

concentration is a feature, not a bug

valuation matters less than duration

policymakers will choose stability over purification

None of these are laws of nature. They are beliefs — reinforced by decades of institutional precedent.

Calling this a “bubble” implies that excess can be isolated and corrected without disturbing the rest. But this isn’t a corner of the market inflating independently.

It’s the load-bearing architecture.

The Bets Being Made Outside the Market

When people talk about a bubble, they are usually reacting to prices. But the more consequential bets today sit outside the market itself — in policy behavior, institutional limits, and social tolerance for distortion.

At a structural level, investors are assuming:

Stability is prioritized over correction

Large dislocations are treated as systemic risks, not cleansing events.Liquidity is political, not cyclical

Support arrives not because markets deserve it, but because instability is unacceptable.Fiscal capacity substitutes for market discipline

Debt expands to bridge shocks markets are no longer allowed to clear.Institutions retain enough credibility to function

Not perfectly, but sufficiently to keep contracts enforceable and collateral trusted.Distortion is tolerated longer than theory suggests

Pressure builds, but rupture is delayed through transfers, regulation, and narrative management.

These are not optimistic assumptions. They are contingent ones.

If This Fails, It Won’t Look Like a Pop

Failure in this framework is unlikely to arrive as a single, dramatic unwind.

More plausibly, it shows up as loss of resolution:

markets that no longer price risk cleanly

volatility that never fully resolves

interventions that arrive earlier and stay longer

correlations that remain high even outside crises

asset prices that rise nominally while confidence erodes

The system still functions — but with increasing friction.

This is not collapse.

It is degradation.

Why “Bubble” Language Misses the Point

A bubble implies excess can be identified, isolated, and removed.

This framework has no such release valve.

If it breaks, it breaks horizontally, not vertically — across assets, institutions, and policy tools at once.

That is why this moment feels ideological rather than analytical. It is not about whether prices are justified, but whether the structure can continue absorbing its own contradictions.

The Uncomfortable Middle Ground

Most investors are not blind believers. They are pragmatic participants.

They recognize the fragility — and still choose exposure — because the alternative is not safety, but disengagement from the system itself.

That is not euphoria.

It is reluctant consent.

And that distinction is what makes this moment different from a bubble.

Why This Makes Traditional Advice Unsatisfying

This framing explains why so much conventional guidance feels inadequate.

There is no obvious “correct” move:

selling everything assumes a viable outside option

staying fully invested feels like blind faith

hedging is costly and imperfect

diversification weakens when correlations converge

The discomfort isn’t about not knowing what will happen.

It’s about realizing there may be no neutral position.

From Prediction to Positioning

Reframing the question helps.

Instead of asking:

Is this a bubble?

A more honest question is:

What am I positioned for if the system holds — and if it strains?

That shift moves the conversation away from calling tops and toward:

liquidity awareness

balance-sheet resilience

time-horizon alignment

optionality over certainty

Believing the system persists is not naïve. Doubting it is not enlightened. Everyone is making a bet — most just don’t articulate which one.

The Quiet Reality

The uncomfortable truth is this:

Most participants already believe the floor exists.

They just don’t like saying it out loud.

Not because it feels elegant — but because the alternative is not a better portfolio.

It’s a different world.

And that’s not a bubble problem.

It’s a belief problem.